Information Disclosure Based on the IFRS Sustainability S2 Disclosure Standards

Basic Concept

The IDEC Group has been conscious of eco-friendliness since its foundation in 1945 through it's “Save all” and “Pursuit of saving” by words. We have formulated “The IDEC Way” in 2019 and have since been maintained a management focus on environmental issues and reduction of environmental impact through the realization of safety, ANSHIN, and well-being. Responding to climate change is a major societal challenge globally.

We identify responding to climate change as one of our priority issues. Having set the Vision for 2030 in the Materiality, we are promoting various initiatives aimed at achieving a sustainable society.

The IDEC Group has disclosed climate-related information based on the TCFD (Task Force on Climate-related Financial Disclosures) since FY2022. This year, we disclose climate-related information based on the IFRS (International Financial Reporting Standards) S2 that succeeds the TCFD recommendations.

Governance

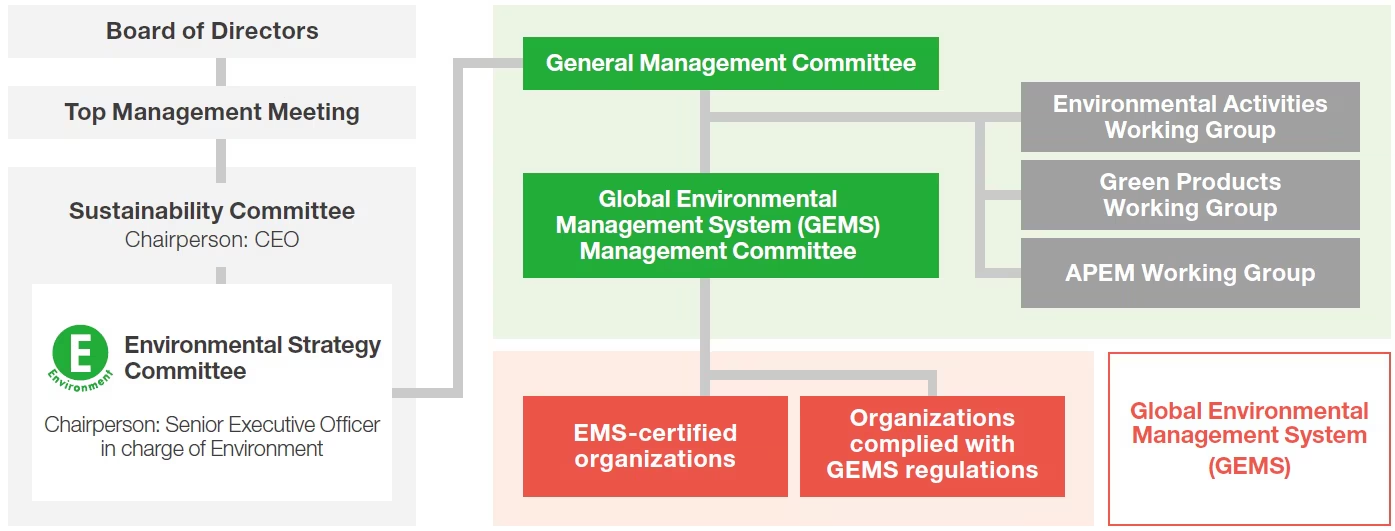

The Environmental Strategy Committee, a specialist committee of the Sustainability Committee chaired by the CEO, plays a key role in our efforts to disclose climate-related financial information.

The Environmental Strategy Committee is composed of employees from various departments, and meets every other month under direction by the Senior Executive Officer in charge of the Environment. Decisions made by the Environmental Strategy Committee are discussed by the Sustainability Committee, reported to the Top Management Meeting for approval, then reported to the Board of Directors for final approval. Progress on the goals set in the medium-term management plan started in FY2026 are reviewed at the meetings every other month, and response measures are discussed if things are not progressing as planned.

As part of our global governance structure, in FY2025 we established and launched a Global Environment Management System Steering Committee. The committee consists of members from IDEC head office, domestic group companies, and bases in Suzhou, Taiwan, and Thailand, and each APEM site (France, UK, Denmark, Tunisia and USA) and holds quarterly Steering Committee meetings. The committee checks progress on environmental issues, shares information on topics such as waste, eco-friendly materials, and the introduction of recycled plastics, and discusses environmental issues.

Framework on the environmental governance

Departments responding to climate change and each role

| Name | Function | Number of Meeting |

| Board of Directors | Supervision of important matters related to climate change | 7 times per year* |

| Top Management Meeting | Decision making of important matters related to climate change | 8 times per year* |

| Sustainability Committee | Review of important items relating to climate change, and submission of those to the Top Management Meeting | Twice a year |

| Environmental Strategy Committee | Management of climate-related opportunities | Once a month |

| Risk Management Committee | Management of climate-related risks | Twice a year |

| Executive Officer in charge | Senior Executive Officer in charge of the environment | |

| Responsible Department | Strategic Planning, Environmental Promotion, Accounting, CSR, HR&GA | |

Climate Resilience

Although the Announced Pledges Scenario (APS) was removed from the key scenarios of the World Energy Outlook 2025 (WEO 2025) and the Current Policies Scenario (CPS) was reinstated—indicating a degree of stagnation in global climate change mitigation efforts—the IDEC Group’s selected scenarios for FY2026 remain the same as in the previous year. For transition risks, we adopted the WEO 2025 Stated Policies Scenario (STEPS, 2.6°C scenario) and the Net Zero Emissions Scenario (NZE, 1.5°C scenario). For physical risks, we adopted RCP2.6 (2°C scenario) and RCP8.5 (4°C scenario). These scenarios were used as references in formulating the IDEC Group’s world view.

Strategy

The IDEC Group regards environmental strategy as an integral part of its business strategy, and has incorporated eco-friendly products into its transition plan starting in FY2026 by introducing sales targets for eco-friendly products as KPIs. This will enable us to systematically improve the level of environmental contribution of our business activities.

We are also accelerating the development of our value chain with suppliers by setting supply chain engagement rate as a KPI and revising CSR procurement and green procurement guidelines. In addition, we are continuously engaged in various environmental initiatives, including reducing CO2 emissions to achieve carbon neutrality, reducing industrial waste, and increasing recycling rates.

These transition plan-related activities align with the IDEC Group's purpose of contributing to the realization of safety, ANSHIN, and well-being for people worldwide, as a harmonized approach to environmental considerations. In addition, ESG-related information, including disclosures based on the TCFD Recommendations, has been included in our Securities Report since of FY2024. As for transition plan, please click here.

Strategy: Climate change risks and opportunities

Centered on the Environmental Strategy Committee, we identified climate-related risks and opportunities that are reasonably expected to affect the IDEC Group’s outlook, with reference to the climate-related risk and opportunity items in the CDP questionnaire, one of the global standards for environmental disclosure.

In doing so, we referenced and considered the applicability of the "Industry-based Guidance on implementing Climate-related Disclosures" (Electrical & Electronic Equipment) defined under the application guidance for IFRS-S2 Climate-related Disclosure Standards. Through this process, we identified transition risks and physical risks, assessed the impacts of climate-related risks and opportunities that are reasonably expected to occur over the short, medium, or long term, identified their potential financial impacts, and defined the relevant time horizons.

Risk management

For each of the climate-related risks and opportunities identified by the Environmental Strategy Committee, we considered the likelihood of occurrence, degree of impact, and amount of potential financial impact, and compiled them into a risk and opportunity map. The identified results and risk items that have been assessed as important in our mapping are managed by referring to an integrated risk map for the IDEC Group. They are also reflected in the risks and opportunities associated with natural capital, one of our materialities.

The Environment Promotion Department lists environmental risk management items on an annual risk management table, specifies performance indicators, and reports the state of achievement to the Risk Monitoring Subcommittee.

Major risk list

|

Category |

No. |

Item |

Potential |

Anticipated risks |

IDEC Group's responses |

|

|

Tran- |

Market | ❶ | Increase in raw material costs | B/E Short, Medium, Long-term |

・Suspension of factory operations and transportation delays due to global natural disasters and human disasters, etc. ・Resulting shortages of parts and materials, and resulting chain of increased transportation, labor, and energy costs ・ Eco-friendly materials, low environmental impact materials and technologies |

・Transfer costs in response to price increases by continuously increasing mutual understanding with suppliers and customers. |

| ❷ | Growing environmental awareness among customers and investors | C/D Medium, Long-term |

・Declining demand and damage to corporate value due to growing criticism of products and initiatives with high environmental impact ・Increased weight of services as a factor in purchasing decisions ・Rapid changes in trends within the industrial products sector ・Declining trust from stakeholders |

・Position environmental strategy as one of the priority items in the medium- to long-term plan, set materiality KPIs relating to the environment, such as increasing the cumulative ratio of eco-friendly products among new products, and check progress. |

||

| Tech- nology |

❸ |

Delay in relative to competitors |

C Medium, Long-term |

・Rapid emergence of new products that generate added value through environmental response in the industrial products sector and increasing customer needs for such products ・Enactment of new regulations on GHG emissions ・Increased risk of industrial equipment failures due to climate change |

・Systematically incorporate technologies that we do not have and integrate them with our core technologies through long-term collaboration with other companies. ・Obtain information at an early stage through regular monitoring of regulatory information, and establish a system that allows for reflection of this information in business strategies and product development ・Enhance the durability of equipment and devices to adapt to extreme weather and global warming caused by climate change |

|

| Regu- ration |

❹ | Tendency of carbon pricing | B/E Short, Medium-term |

・Accelerated global momentum for climate change measures and reduced CO2 emissions, with governments around the world introducing carbon taxes ・Introduction of carbon pricing in Japan (from 2028 onward), with carbon taxes being added to energy prices, leading to increased manufacturing costs for raw materials ・Decline in profitability due to stricter regulations and mandatory energy conservation targets |

・Plan and implement planned upgrades to energy-saving equipment. ・Reduce indirect costs through efforts to save energy and improve the operating rate of factories. ・Drive decarbonization activities through the introduction of ICP. ・Invest in technologies necessary for reducing emissions, and introduce a system for regularly managing emission reduction targets |

|

|

Physi- |

Urgent or chronic |

❺ | Natural disasters and temperature rise | D Short, Medium, Long-term |

・Increased frequency of natural disasters such as localized heavy rainfall, cyclones, hurricanes, and typhoons caused by global warming, and extreme changes in rainfall and weather patterns ・Decline in production activities (power shortages, equipment damage, inability of employees to come to work, etc.) and supply chain disruptions due to frequent occurrence of disasters such as abnormal weather conditions worldwide ・Spread of new viruses and other infectious diseases due to climate change ・Increased cooling costs and decreased productivity due to rising temperatures, and disruption of transportation networks due to prolonged cold weather |

・Enhance BCP measures to enhance the company's resilience. ・Assess and review to supply chain risks. ・Prepare hazard maps of manufacturing sites and find potential risks, and formulate disaster prevention plans tailored to each region ・Formulate recovery plans for each site and develop manuals for employee work procedures ・Diversify production bases for mainstay products |

A: Increase in direct costs B: Increase in direct and indirect costs C: Reduced sales due to decreased demand for products and services D: Reduced sales due to decreased production capacity E: Increase in capital expenditure

Timeframe: Short: less than 3 years, Medium: between 3 and 5 years, Long: over 5 years

Major opportunity list

| Category | No. | Item | Potential financial impact | Anticipated opportunities | IDEC Group's responses |

| Resource efficiency | ❶ | Demand for low-emission products and a diverse variety of new products and services through R&D and technological innovation | B/A | ・Increased demand for recycling accompanying effective utilization of resources ・Increased demand for products with low emissions throughout the product life cycle ・Political measures such as GX bonds and subsidies ・Selection of suppliers based on the extent of GHG emissions reduction | ・Accelerate technological innovation taking environmental aspects of main product lines into account ・Research applications of easily recyclable materials to products ・Secure a first-hand advantage by accelerating investment in development ・Introduce Life Cycle Assessments (LCA) |

| ❷ | Shift to alternative materials / diversification / new technologies | B | ・Increased demand for new technological innovations to address various changes in working environments caused by climate change ・Diversification of working environments and development of unmanned and remote technologies due to the decline of the working-age population ・Popularization of robots in harsh and dangerous working environments ・Increased sales of automation systems driven by demand for labor reduction | ・Shift away from extrapolations of existing technologies ・Engage in M&A and business alliances, strengthen software and system-related technologies through recruitment and training of human resources ・Promote the incorporation of new technologies to respond to diverse needs through partnerships and collaborations with other companies and academic organizations. ・Develop products utilizing HMI and sensing technologies, and propose solutions through systematization and packaging. | |

| Products and services | ❸ | Transition to distributed energy generation and the creation of new markets | A | ・Progress in transition measures in response to global climate change ・Utilization of clean energy other than electric power, and increased demand for labor-saving technologies and energy-saving products ・Launch of various renewable energy development and energy conservation projects as measures to reduce emissions | ・Enter new markets, engage in technological innovation, and secure competitive advantages ・Develop products utilizing HMI and sensing technology, and propose problem-solving solutions based on the needs of new markets. ・Implement localization strategies that provide products and services tailored to regional characteristics |

A: Increased sales through entry into new and developing markets B: Increased sales as a result of increased demand for products and services

Timeframe: Short: less than 3 years, Medium: between 3 and 5 years, Long: over 5 years

The world images assumed in each scenario are summarized as below.

The Image of the world in +1.5℃ and 2℃

Transition Risks | Great increase carbon tax (carbon price) |

Opportunities associated with Transition | Business opportunity for new energy |

Physical Risks | Increase temperature (+2.0℃) |

The Image of the world in +4℃

Transition Risk | Increase movement restriction |

Opportunities associated with Transition | Develop and prevail protective clothing for environment |

Physical Risks | Great increase temperature (+4.0℃) |

Metrics and targets

The IDEC Group aims to achieve carbon neutrality by 2050. To reduce CO2 emissions, in our sustainability KPIs we have set the targets of reducing Scope 1 and Scope 2 CO2 emissions by 35% by FY2028 and 50% by FY2031 (both compared to FY2020).

Regarding the internal carbon price (ICP), which was introduced in FY2023, we set the price at ¥14,000 per ton, unchanged from FY2026. While the impact of ICP on environmental investment decision-making is not yet sufficient, the Environmental Strategy Committee is working to raise awareness within the Group by introducing model cases of ICP utilization on the intranet.

Our return on carbon (ROC) profit ratio, which indicates how much CO2 was reduced and how efficiently profits were earned, has continued to decline in line with the decrease in operating profit since FY2024. However, in FY2026, ROC improved significantly, reflecting the increase in operating profit.

With the Performance Share Units (PSUs) introduced into the executive compensation system in FY2024, approximately 10% of compensation may be allocated to directors and executive officers in the form of common stock, with non-financial indicators being used in the calculation of PSUs. Non-financial indicators used in the calculation of PSUs include CO2 reduction ratio. Our return on carbon (ROC) profit ratio, which indicates how much CO2 was reduced and how efficiently profits were earned, has continued to decline in line with the decrease in operating profit.

As for CO2 emissions in FY2026, Scope2 increased, reflecting the recovery in sales. CO2 emission intensity, Scope1 and Scope3 decreased compared with FY2025.

As for the initiatives in FY2026, the on-site solar power generation equipment introduced at Tatsuno Distribution Center has begun operation and contributed to reducing CO2 emissions. Going forward, we will continue our efforts to achieve our new sustainability KPIs and reduce CO₂ emissions by considering the global installation of solar power generation facilities, switching to electricity with lower emission factors, and achieving improved operating rates at each factory.

Information disclosure based on TNFD

The IDEC Group's environmental-related disclosures have been aligned with IFRS S2 since 2024, but stakeholder demands are expanding from climate change to include biodiversity and TNFD.

Therefore, starting in fiscal 2025, we have begun preparations to disclose information aligned with the TNFD framework and to identify nature-related issues using the LEAP approach for risk and opportunity assessment. Utilizing LEAP, we disclose information aligned with the four elements of the TNFD framework: governance, strategy, risk and impact management, and metrics and targets.

Governance

The board of directors oversees important sustainability matters such as TCFD and TNFD. The Environment Strategy Committee, one of the specialized committees of the Sustainability Environmental Strategy Committee, takes the lead in conducting analysis and evaluation regarding nature-related risks and opportunities, dependencies, and impacts. For further information, please click here.

Strategy

To clarify the relationship between our business activities and their dependencies and impacts on nature, we conducted a materiality assessment using the external tool ENCORE. While the dependency and impact items identified by ENCORE represent industry-wide, general items, some of them did not fully reflect the specific characteristics of our business activities. Accordingly, from the results of the materiality assessment, we identified water supply as a key dependency, and CO₂ emissions as well as the discharge of hazardous pollutants into water and soil as key impacts that are highly relevant to the IDEC Group’s business activities. Based on ENCORE’s analysis, we identified four types of natural capital on which the IDEC Group’s business activities depend: water, soil, biodiversity, and minerals.

Dependency and impact on natural capital

| Natural capital | Dependency | Impact | Factors that have impact | |||||

| Atmosphere | Low | Low | Weather conditions, drought, changes in ocean currents, and circulation | |||||

| Land geomorphology | Medium | Medium | Floods, earthquakes, landslides | |||||

| Minerals | Medium | Medium | Changes in Land/Freshwater/Seabed | |||||

| Ocean geomorphology | Changes in Land/Freshwater/Seabed | |||||||

| Soils and sediments | Low | Low | Changes in Land/Freshwater/Seabed, changes in pollutant concentration, changes in species composition | |||||

| Species | Changes in diseases, species composition, and weather conditions | |||||||

| Structural and biotic integrity | Medium | Medium | Floods, changes in land/freshwater/seabed, fires | |||||

| Water | Medium | Medium | Drought, changes in pollutant concentrations, sea level rise | |||||

Risk and impact management

In considering nature-related risks and opportunities, we conducted risk and opportunity workshops in Japan, China, Taiwan, and Thailand in FY2027. During these workshops, we discussed the IDEC Group’s dependencies on and impacts on natural capital, as well as related risks and opportunities associated with our business activities.

Major nature-related risks

| Classification | Item | Responses | ||||||||||||

| Physical risks | Acute | Operational shutdowns at key suppliers; disruptions to logistics and supply chains (floods, typhoons) | BCP development, securing alternative sourcing, inventory strategy, and utilization of cloud technologies | |||||||||||

| Heat stress among workers due to rapid increases in temperature and humidity | Heat stress prevention measures (salt tablets, hydration, cooling garments) | |||||||||||||

| Chronic | Declines in productivity and quality due to deteriorating working conditions caused by rising temperatures | Improvement of air conditioning and ventilation systems in factories and workplaces | ||||||||||||

| Reduced production volumes due to power usage restrictions resulting from fossil fuel depletion | Transition to component/material specifications designed for high-temperature environments | |||||||||||||

| Transition risks | Policy | Stricter regulations on mineral resource extraction, restrictions on use, and import/export controls due to mineral depletion | Diversification of suppliers, use of recycled materials, and monitoring of policy developments | |||||||||||

| Assessment and use of recyclable materials, implementation of usage restrictions, and review of procurement practices | Switch to low-carbon electricity and environmental management systems (ISO 14001) | |||||||||||||

| Market | Investment avoidance due to deterioration in ESG ratings, increased environmental requirements from customers, and suspension of business transactions | Promotion of ESG Management and Enhancement of Environmental Information Disclosure | ||||||||||||

| Demand fluctuations and shifts in customer requirements; surge in global mineral prices (copper and rare metals) | Ongoing monitoring of mineral and metal markets and revision of pricing contracts | |||||||||||||

| Technology | Technological obsolescence due to environmental requirements: delays in the transition to energy-efficient equipment and low environmental impact materials | Development of a technology strategy Strengthening of R&D investment Promotion of the development of eco-friendly technologies Technical collaboration with external partners |

||||||||||||

| Obsolescence of existing products due to the emergence of resource- and energy-efficient competing technologies | ||||||||||||||

| Reputation | Reputational damage and social media backlash from inadequate waste and chemical management | Strengthened supply chain management and development of a supplier code of conduct Conduct of environmental and human rights due diligence |

||||||||||||

| Liability | Litigation and liability risks associated with environmental pollution, ecosystem damage, and water and soil contamination | Environmental regulatory compliance and operation of an environmental management system (ISO 14001) Enhanced waste management, strict wastewater control, and regular internal audits Establishment of an emergency response system |

||||||||||||

Major Nature-Related Opportunities

| Classification | Item | Responses | ||||||||||||

| Corporate performance | Market | Rising demand for eco-friendly products (eco-friendly materials, products with low water and CO₂ use, low energy consumption, and high resource efficiency) | Environmental certification, manufacturing technology development, investment, energy-saving proposals for customers, and enhanced R&D of eco-friendly products | |||||||||||

| Revenue opportunities from early development aligned with market trends | Solution-based sales aligned with customers’ ESG and environmental initiatives | |||||||||||||

| Resource efficiency | Cost savings from improved water and energy efficiency in operations | Introduction of renewable energy | ||||||||||||

| Reduced use of copper, aluminum, and rare metals in development, and use of recycled materials | Consideration of alternative materials and establishment of recycling loops | |||||||||||||

| Products and services | Proposal-based business for optimizing energy efficiency across entire production lines | Packaging of “energy savings visualization” and “optimal robot control” | ||||||||||||

| Increasing interest in environmentally friendly products | Bio-based materials R&D and enhanced sensor technologies | |||||||||||||

| Capital flows and financing | Growing subsidies and incentives for investment in high environmental performance equipment | Utilization of subsidies for the introduction of energy-efficient equipment (METI and MLIT) | ||||||||||||

| Reputational capital | Enhanced brand value as an environmentally responsible company | CSR activities and supplier engagement | ||||||||||||

| Sustainability Performance |

Sustainable use of natural resources | Sustainable procurement through the use of recycled materials (copper and plastics) | Use and evaluation of recycled materials | |||||||||||

| Expansion in the use of certified and recycled materials | Continuation of ongoing initiatives: establishment of green procurement standards, preferential use of certified materials, installation of solar panels, and purchase of renewable electricity | |||||||||||||

| Ecosystem protection, restoration, and regeneration | Increased customer selection as a company promoting ecosystem-conscious practices | Formulation of procurement policies that consider ecosystems (e.g., zero deforestation) | ||||||||||||

| Contribution to local communities through greening and ecosystem restoration within and around sites, as well as measures against invasive species | Biodiversity surveys, environmental restoration projects, collaboration with local governments and communities, installation of biotopes and eco-stacks, removal of invasive plant species, and vertical greening | |||||||||||||

Major dependencies and impact by natural capital

| Natural capital | Major Dependencies | Major Impact | |||||||||||||

| Water resources | Manufacturing water use (molding, cooling, cleaning, chemical processes, etc.) | Impact on depletion due to water resource use | |||||||||||||

| Water resource depletion due to overuse | Impact on rivers, ponds, and other water bodies due to wastewater discharge from septic tanks | ||||||||||||||

| Water use for domestic purposes | |||||||||||||||

| Soil | Land use for factories and offices | Impact on ecosystems due to soil degradation and land-use change | |||||||||||||

| Soil associated with on-site and facility landscaping | |||||||||||||||

| Biodiversity | Wood materials (cardboard, crates, pallets) | Impact on biodiversity through deforestation, excessive water use, water pollution from effluent, and species decline due to habitat destruction associated with pulp production in the supply chain | |||||||||||||

| Impacts on biodiversity from the use and disposal of timber materials and hazardous substances | |||||||||||||||

| Impacts of pulp production on forests and water | Impact on biodiversity due to the unintended use or disposal of hazardous substances | ||||||||||||||

| CO₂ emissions from manufacturing energy use | |||||||||||||||

| Metal and mineral resources | Supply chain dependence on metals and mineral resources | Impact on depletion of metals due to component use | |||||||||||||

| Dependence on petroleum‑based resins and insulation materials | Pressure on natural resources due to material use | ||||||||||||||

| Use of metals in component manufacturing and depletion risk | Residual accumulation of non-biodegradable metal waste disposed of as industrial waste | ||||||||||||||

| Upstream environmental impacts associated with component procurement (including soil erosion, water pollution, and ecosystem degradation) | |||||||||||||||

| Atmosphere | Use of sunlight for solar power generation | Greenhouse gas emissions resulting from the use of electricity and fuels | |||||||||||||

| GHG emissions from electricity and fuel use | Greenhouse gas emissions from commuting by private vehicles | ||||||||||||||

| Land geology | Petroleum consumption from plastic packaging use | ー | |||||||||||||

| Fossil fuel extraction for power generation | ー | ||||||||||||||

| Marine geology | Supply chain marine transport and port use | ー | |||||||||||||

| Port use and seabed resource extraction | ー | ||||||||||||||

Metrics and Targets

As measurable indicators in IDEC's business activities, we selected four items from the measurement indicators defined by the TNFD.

TNFD's measurement indicators on dependencies and impacts

| Measurement Indicator No. | Drivers of Natural Change | Indicator | Measurement Indicator | Relevant Elements in IDEC | |||||||

| Climate change | GHG emissions | Refer to ISSB's IFRS S2 "Climate-related Disclosures" | CO2 Emissions | ||||||||

| C3.0 | Resource use/ replenishment | Intake and consumption from water-scarce regions | Water withdrawal and consumption70 (m3) from areas of water scarcity, including identification of water source. | Water consumption by site and total | |||||||

| Measurement Indicator No. | Drivers of Natural Change | Measurement Indicator | Relevant Elements in IDEC | ||||||||

| C7,2 | Risks | Description and value of significant fines/penalties received/litigation action in the year due to negative nature-related impacts. | Non-financial indicators listed on IDEC Integrated Report | ||||||||

| C7.4 | Opportunities | Increase and proportion of revenue from products and services producing demonstrable positive impacts on nature with a description of impacts. | Sales of enhanced eco-friendly products | ||||||||